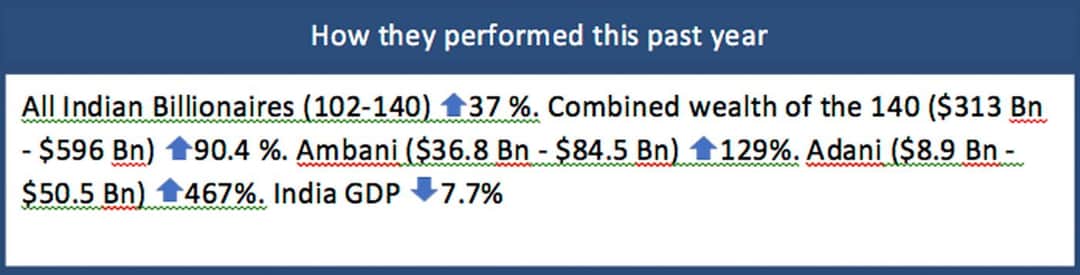

The ranks of Indian Dollar Billionaires swelled from 102 to 140 in 12 months, if the Forbes 2021 List is to be believed (and when it comes to billionaires and their wealth, Forbes is mostly to be believed). Their combined wealth, it notes, has “nearly doubled to $ 596 billion” in just the past year.

This means 140 individuals, or 0.000014 per cent of the population, had a cumulative worth equivalent to 22.7 per cent (or well over a fifth) of our Gross Domestic Product of $ 2.62 trillion, bringing, as they always do, that whole other meaning to the word 'Gross'.

Most major Indian dailies carried the Forbes pronouncement in that approving tone they reserve for such feats – omitting to mention what the Oracle of Pelf says in a more upfront and honest way.

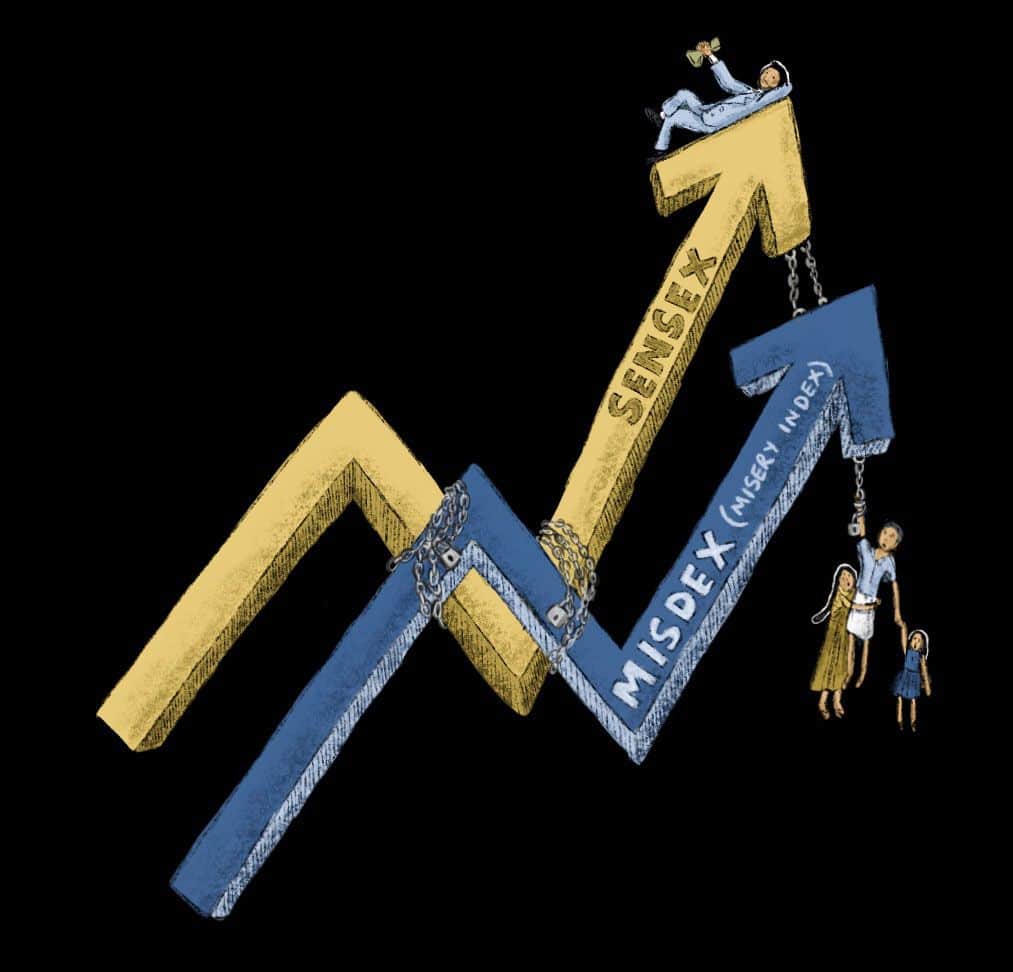

“Another Covid-19 wave,” says Forbes in the first paragraph of its report on this country, “is sweeping across India and total cases now exceed 12 million. But the country’s stock market has shrugged off its pandemic funk to scale new peaks; the benchmark Sensex is up 75% from a year ago. The total number of Indian billionaires rose to 140 from 102 last year; their combined wealth has nearly doubled to $ 596 billion.”

Yup, that combined wealth of these 140 plutocrats went up by 90.4 per cent – in a year when GDP contracted by 7.7 per cent. And the news of these achievements comes in as we watch a second wave of migrant labourers – once again in numbers too large and dispersed to seriously enumerate – leaving the cities for their villages. The resultant job losses won’t do the GDP any good. But mercifully, shouldn’t harm our billionaires too much. We have Forbes’ assurance on that.

Besides, billionaire wealth seems to work in inverse logic to Covid-19. The greater the concentration, the less the chance of any super-spreader effect.